If our present-day world – one already bursting with uncertainty, volatility and geopolitical mayhem – is not in need of one thing, it surely is a stiff dose of financial turmoil. With several bubbles being blown every day now, the probability of that kind of turmoil popping up is unfortunately closer to 100 percent than it is to 0 percent. But not all bubbles are the same.

Anybody involved, remotely or closely, with the world of finance should have one book always close at hand. In 2011 Carmen Reinhart and Kenneth Rogoff published their opus magnum This Time Is Different with the under-title Eight Centuries of Financial Folly. The most important conclusion Reinhart and Rogoff reached was that history repeats itself as far as financial crises are concerned. During the eight centuries of financial excesses, they studied those closely involved in what led to financial crises, the ‘experts’, claimed almost every time that “this time is different” and that it was absolutely wrong to conclude that what looked this time around like the prelude to a new financial crisis was a “misunderstanding” or “cheap panic-mongering” or “sheer stupidity”. But time and again the ‘experts’ were proven wrong: this time was not different, the same type of omens led to the same type of financial crises.

Are we today once more in that kind of situation? Are we again confronted with financial excesses or bubbles while in the background ‘experts’ shout that “this time is different”? My answer to these questions is a “nuanced yes”. I see presently two bubbles and one case of financial excess around us. The first bubble is the crypto currency market that I define as a bubble pur sang. I distinguish between cryptocurrencies on the one hand and stablecoins and ARTs (Asset Reference Tokens) on the other hand. The two latter have intrinsic value, although confidence in them should be of the very watchful kind.

“The same type of omens led to the same type of financial crises”

The second bubble is the artificial intelligence rage that can best be described as a development that will change the world but not after passing through a bubble bursting or, if you want, cleansing phase. Out of the process of Joseph Schumpeter’s creative destruction, the productive and profitable AI remnants will rise like giants (and change the world).

The financial excess situation, or, if you want, the third bubble, is to be found in the private credit market recently defined by Jamie Dimon, the CEO of the premier bank of the world JP Morgan Chase, as a “recipe for a financial crisis”.

Bubble pur sang

What is a bubble? A commonly used definition is that in a bubble the prices of the assets concerned exceed their fundamental value, being the current valuation of the expected stream of future payoffs that these assets will generate, in a significant way. This definition immediately introduces a significant degree of uncertainty because the expected stream of future payoffs is by definition an uncertain value that depends on one’s valuation.

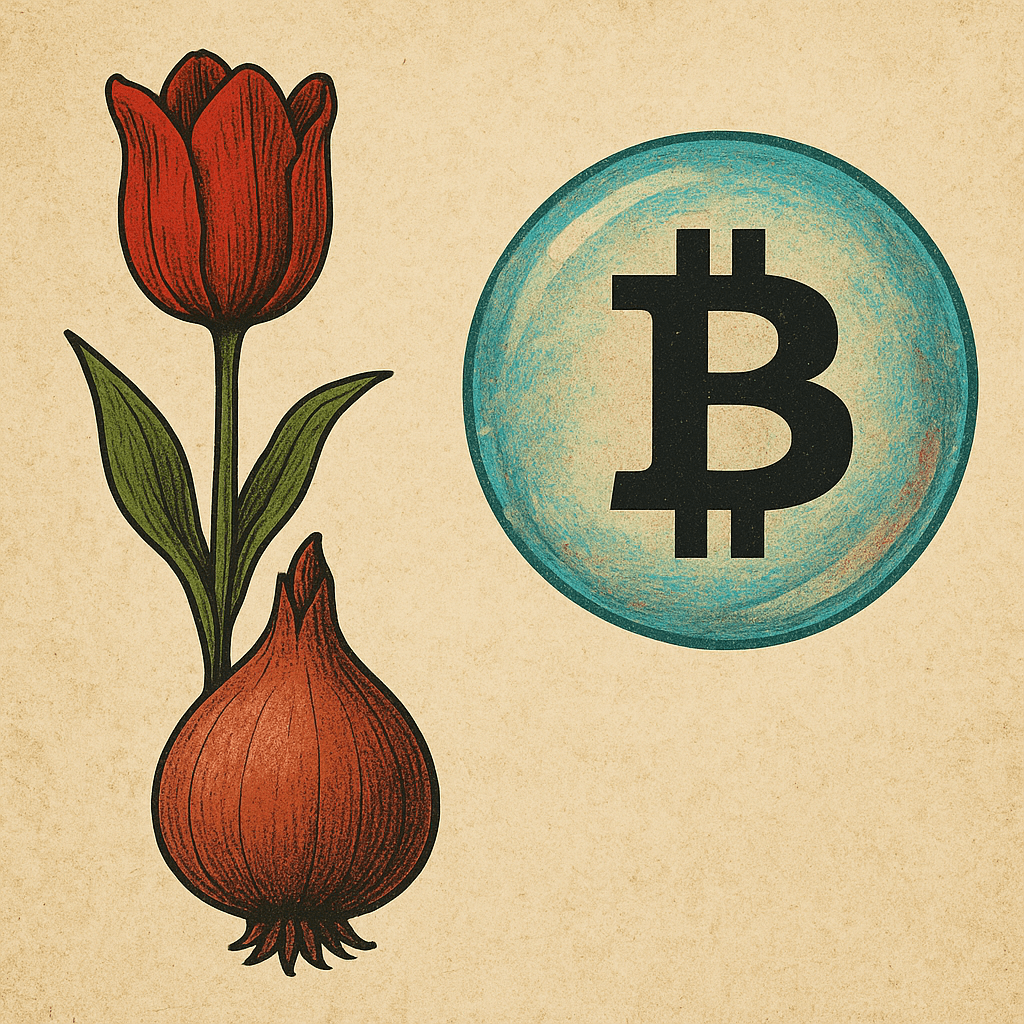

Despite this uncertainty, I define the crypto market as a bubble pur sang. No doubt about it. Why? For the simple reason that cryptocurrency assets offer no underlying value because such assets do not generate payoffs (cash flows, profits) for those who hold them. The current value of cryptocurrencies depends entirely upon the expectation of greater resale value. If this expectation turns negative, crypto’s values drop as already happened frequently. In contrast with, for example, gold, cryptocurrencies have also no value whatsoever as possible inputs in other production or supply chains. The crypto bubble is comparable to the bubble of all bubbles, the Dutch tulip mania of the 1630s when the price of tulip bulbs went so high that there was no relation whatsoever anymore between that price and the payoff-generating capacity of those bulbs.

“Cryptocurrency assets offer no underlying value because such assets do not generate payoffs”

Half September of this year Arjun Sethi, the CEO of Kraken, one of the largest crypto exchanges declared that, yes indeed, we’re in the midst of a crypto bubble (Yahoo Finance, September 11, 2025). Around the time of Sethi’s remarkable confession the total market capitalization of all cryptocurrencies crossed for the first time the $4 trillion threshold. At the moment of writing the market capitalization of Bitcoin alone is $2.4 trillion, with Ethereum as distant second of the cryptocurrencies with a market value of $520 billion. To put this in perspective, note that Bitcoin alone is worth more than the combined market value of Oracle, J.P. Morgan Chase and Walmart. Or: Bitcoin and Ethereum together are considered more valuable than Exxon Mobil, Johnson & Johnson, Samsung, Procter & Gamble, SAP, General Electric, Coca Cola and Novartis taken together.

Sounds ok, yes? Or not?

Despite the purely speculative nature of crypto values, regulation has distinctly turned pro crypto in the United States, not least under the influence of the involvement of president Trump and his family in different crypto adventures like with the staggering issuance of presidential meme coins from which the president Trump made at least $350 million. Some of us remember that Donald Trump held a very negative view on cryptocurrencies during his first presidential term. Furthermore, we are now at a point where also traditional companies are creating their so-called “digital asset treasuries” through which they load up on cryptocurrencies to boost their liquidity position and share price. Let me be polite and describe this strategy as ‘playing with fire’, although stronger wording would be more appropriate.

A last point to note with respect to cryptocurrencies is the close involvement of the criminal world, most of all because of the anonymity of cryptos. It is certainly true that some crypto financial streams became easier to trace by the authorities (read Andy Greenberg’s Tracers in the Dark, 2024), that major darknet platforms were taken down and that financial crime units constantly upgrade their technology and know-how but nevertheless huge sums still pass through cryptocurrencies related to payments for ransomware, money laundering, credit card scams, massive Ponzi schemes, payments for major drug deals and other sorts of illegal activities.

There is much truth in the claim made by Jemima Kelly, a Financial Times commentator: “Crypto has never been about innovation but about getting away with things you would not otherwise be able to do. And it’s not just the US. While Ireland has banned political crypto donations, Nigel Farage’s Reform party just became the first major UK party to accept them, opening the door to all sorts of actors exerting political influence. Crypto was built for this. Murky deals aren’t the bug, they are the whole point”.

“Disruptive discontinuity”

Increasingly the investment rage in Artificial Intelligence (AI) is also considered to be a bubble. In a recent note the research firm MacroStrategy Partnership calculated that the bubble in AI is 17 times larger than the dot-com bubble that developed at the end of the 20th century and 4 times larger than the 2008 global real estate bubble. Despite the indeed enormous sums invested now in AI – think in rounded numbers of more than $500 billion a year – we have to be more nuanced here. I’m not arguing that “this time is different” but there is some truth in the claim of Jeff Bezos, the big boss of Amazon, that AI is “a good kind of bubble … an industrial bubble as opposed to financial bubbles … the benefits to society from AI are going to be gigantic. Investors have a hard time in the middle of the present excitement distinguishing between the good ideas and the bad ideas … (but) … AI is real, it is going to change every industry”.

Yes, AI will change every industry, but it will have to go through a process succinctly described by William Janeway, professor of economics at the University of Cambridge (UK) and author of the sublime book Doing Capitalism in the Innovation Economy (2018) in which he documents the fact that bubbles are often central to the adoption of new technologies. In a recent column on Project Syndicate (August 29), Janeway writes: “The histories of the railroads, electrification, and the internet are relevant for AI. Each required massive investments in physical infrastructure before anyone discovered viable, scalable applications for the new technology. Today, we take these industries for granted, forgetting that their evolution featured serial bankruptcies and a wide range of supportive state interventions to protect competitors from themselves. As so often happens, rational individual responses generated hugely destructive coordination failures. Through it all, massive speculative capital flows funded the construction of these transformational networks in a process punctuated by episodic financial crises … Once again, capital must flow into assets whose economic value cannot be known in advance. For the AI bubble to deliver long-term, economic stable, financially rewarding results without disruptive discontinuity would be unprecedented in the history of capitalism”.

A long quote that – so I strongly believe – says it all. AI investments in the US alone amounted to close to $500 billion this year, with the real number of these investments even higher because, as The Economist has documented, the so-called ‘hyperscalers’ are using different accounting tricks to hide away some of their AI spending. These hyperscalers are Oracle, Microsoft, Meta, Amazon and Google, several of them teaming up with Sam Altman’s Open AI, the firm that created ChatGPT. Altman on different occasions stressed he was not interested in “cost discipline” and that becoming profitable is “not in my top-10 concerns”. The share prices of these hyperscalers and some other AI-linked companies like Nvidia went through the roof as a consequence of FOMO, the Fear Of Missing Out on the hugely uncertain payoffs of AI developments. This equity market frenzy is hence part of the AI rage bubble.

“ Yes, AI will change every industry, but it will have to go through a process”

In this massive AI investment drive huge sums are invested in advanced chips and data centers that will require massive amounts of energy. Morgan Stanley analysts estimate that global spending on data centers and other AI infrastructure will amount to $3 trillion in the coming five years. The basic question is whether the expected payoffs from this investment tsunami are in line with the cost of the infrastructure built-out. At the moment they are not, big time. The AI adoption rate by consumers and corporates shows considerable hesitancy. So there will be tears: some investors will have to face huge losses. Goldman Sachs chief David Solomon argued recently that when the current cycle of AI investment ends “there will be lot of capital that was deployed that didn’t deliver returns. It is not different this time.”.

“So there will be tears: some investors will have to face huge losses”

Will these losses be in the equity sphere or more in the debt sphere? The answer to this question is crucial because, as Reinhart & Rogoff also discovered in their journey through eight centuries of financial folly, the more debt-financed a bubble is, the more disruptive the bursting of the bubble will be for the financial markets and the real economy. The dot-com bubble resulted in only a little contagion because debt played a minor role in the development of the bubble. AI investment tended to be largely equity-financed until now but given the sums involved debt will inevitably become more important as we go along. So the sooner the Schumpeterian creative destruction takes place, the better.

Into the darker corners

My third bubble-related concern is to be found in the so-called private credit market or, as the more technical jargon goes, the non-bank financial intermediaries (NBFIs). The growth of these NBFIs since the Great Financial Crisis of 2008 is to a large extent linked to the stricter regulation imposed on the traditional financial sector in the slipstream of the GFC and to the general climate of low interest rate (despite the uptick in interest rate with inflation outburst in the early 2020s).

NBFIs raise money from investment funds, insurers, pension funds and wealthy investors in search for higher returns, given the level of interest rates in the economy. The role of the NBFIs or non-bank financial intermediaries has grown from a rather insignificant corner of finance to representing a market estimated at somewhere between $2 trillion and $2.5 trillion and growing fast whereas in 2020 that was barely $1 trillion. In the US NBFIs accounted in 2023 for 7% of total corporate credit and while in Europe that number was substantially lower at 1.6%. This alternative finance, as some also label it, focuses on asset-backed financing, be it of the financial kind (consumer finance, small business financing) or the more hard asset kind (airplanes, equipment, residential real estate).

The risks involved in this huge expansion of NBFI-activity are basically twofold. First, there seems to be more readiness to take on board more risky financing. This has to a substantial degree to do with the fact that there is a lot slicing, dicing and repackaging of the loan portfolio going on. JP Morgan analysts estimated that asset managers have created so far $380 billion “collateralized loan obligations” in 2025. In such an intense securitization process a tendency to obscure the real risks involved is a real and present danger. Second, there’s the question of the involvement of traditional banks in the exponential growth of the private credit market. A recent study by the BIS, the Bank for International Settlements or the central bankers’ bank, concluded in a tongue-in-cheek way that we really don’t know how far that involvement of traditional banks really goes.

The bankruptcy of First Brands in the US is a first important signal that large risks are floating around in that private credit market. It is hence not a coincidence that ECB president Christine Lagarde recently warned for what is lurking in the “darker corners of finance”. More specifically she urged to beef up regulation for non-banks such as hedge funds, private equity and insurers, conveniently forgetting to mention the role relatively low interest rates are playing in the expansion of private credit markets.

Rüdiger’s wisdom

Unfortunately, the clouds hanging over financial markets are not limited to the three bubble-ish developments discussed in this blog. Talking to fund managers and representatives of important investment houses, the feeling of increasing alarm about bubbles, debt sustainability – in the EU as well as in the US and Japan – and the degradation of political institutions and norms in the US is widespread and rising. I’m reminded here of a dictum by Rüdiger Dornbush, a brilliant macroeconomist who died all too young (1942-2002) and once claimed that “in economics, things take longer to happen than you think they will, and then they happen faster than you thought they could”.