How Reality Catches Up with Trump

The bond market, the hiccups of Corporate America and the rare earth hardball China played during the trade talks forced American president Donald Trump to adjust his policy agenda significantly. Enjoy this triple bite into a FETA dish.

Donald Trump is the democratically elected president of the United States of America, still the largest and most innovative economy and military most powerful country in the world. Probably none of his predecessors injected so much mayhem and turmoil into the world and into his own country than this 45th and 47th president of the US did during his first six months in the White House. Aggressive rhetoric, constant flip-flopping, and a striking lack of thoughtfulness — traits fundamentally at odds with the dignity of high office — too often defined the words and actions of the second Trump Administration. Donald Trump often speaks and acts as if nothing or nobody can oppose or stop him.

But at least three times during his now almost completed half year in the White House it has become crystal clear that there are forces that even Donald Trump has to take seriously.

Forces Even Trump Acknowledges – FETA

Financial Times journalist Robert Armstrong coined the term TACO (“Trump Always Chickens Out”), I would like to add to our Trump era vocabulary the acronym FETA (“Forces Even Trump Acknowledges”). The Mexican taco tortilla and the Greek feta cheese are delicious ingredients for a summertime meal. Whether they will work out in the enjoyable way in the Trump cuisine remains to be seen.

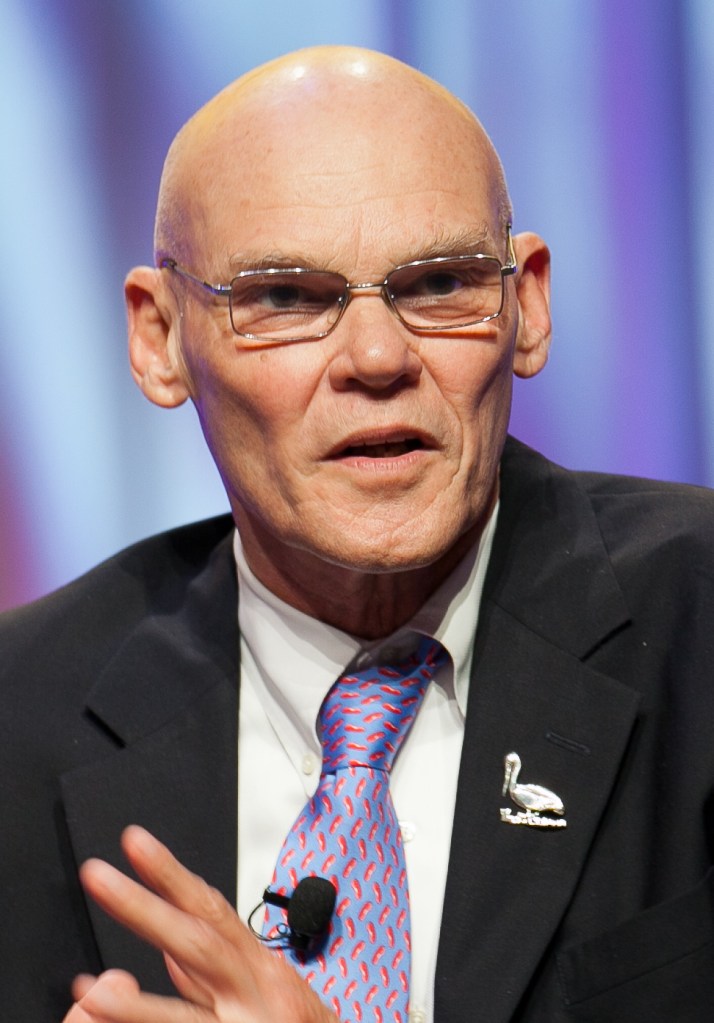

“I used to think that if there was reincarnation, I wanted to come back as the president or the pope or a . 400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.” (James Carville)

The first of these forces is also at the end of the day probably the most powerful of the three. Politicians and their governments should never forget the by now legendary warning of James Carville, the main political advisor of president Bill Clinton, who once quipped that rather as the next US president or a baseball player, he wanted to be reincarnated as the bond market because then “you can intimidate everybody”. In the days after April 2 when Trump launched his trade war and declared this date to be the US’ “Liberation Day” financial markets reacted virulently. US Treasuries (bonds), equities and the dollar were massively sold off promptly feeding fears of a broad financial crisis, not only in the US but also by foreigners. $ 19 trillion of US equities, $ 7 trillion of US treasuries and $ 5 trillion of US corporate bonds are owned by foreigners. The simultaneous sell-off of American bonds and equities and of the dollar is a most unusual combination. A more pronounced vote of mistrust in the Trump policies by the financial markets is hard to imagine.

Apparently it was most of all the sharp sell-off in the bond market that truly frightened president Trump and Scott Bessent, the Secretary of the Treasury. The perspective of the US getting into real trouble with its financing – and the financing needs of the Trump Administration are huge – and risking to see its dollar power seriously eroded was even for the most outspoken pundits of the Trump Administration a bridge too far. Trump reacted by announcing a 90-day pause in the execution of his tariff threats to practically every country in the world. A number of tariff exemptions were also promptly announced. In the meantime Trump even pointed to a further extension of the deadline beyond the present expiry date of July 8 for countries negotiating in “good faith” with the American negotiation team.

James Carville was once again proven right. Although he vehemently denied in public that fear and even panic had shaken the White House, Donald Trump felt truly intimidated by the bond market. Let that, by the way, also be a clear warning for politicians elsewhere in the world, not least within the European Union, who today are first in line to criticize the American president but are themselves ignoring the real possibility that their own lack of sufficiently decisive policy intervention to control the debt escalation and to stimulate economic growth structurally may, and most probably will, one day set those bond vigilantes back into action.

“Donald Trump felt truly intimidated by the bond market. Let that, by the way, also be a clear warning for politicians elsewhere in the world, not least within the European Union“

Corporate messaging

The second force to which Donald Trump lends his ear to, if not to surrender to, is the voice of Corporate America. Together with the vigilantes of the bond market many of the big and not so big shots of Corporate America came into action after “Liberation Day”. As a top executive of a Wall Street bank anonymously told the Financial Times: “Trump has always been disruptive and we all underestimated the level of disruption – we are all just awakening to this”. Although most warnings concerned the risks associated with the tariff and trade war, also Trump’s attacks on the independence of the Fed (the American central bank), on the rule of law and on the heavy handed approach towards major universities like Harvard and Princeton figured on Corporate America’s speaking points.

Several representatives of Corporate America openly warned the president that the policies he was pursuing would backfire strongly, not least for the United States itself. JP Morgan’s CEO Jamie Dimon argued that America’s economic pre-eminence could come under threat from the president’s attempt to reshape global trade. Also Apple’s Tim Cook and Harold Hamm, the billionaire shale gas and oil magnate, openly voiced unambiguous warnings on the ultimate consequences of the Trump policies. But most CEOs, like for example those of the car industry, Walmart and Home Depot, talked more secretly to the president, well aware of the fact that private persuasion works better with this president than public outcries. They also often send back-channel messages to Treasury Secretary Scott Bessent, generally considered to be one of the most moderate Trump trustees.

China’s stronghold

On June 10 president Trump announced with his usual bravado that the United States and China had reached a deal to restore their trade war truce. “Our deal with China is done”, Trump enthusiastically announced on his Truth Social network. It does, however, not take a demanding analysis to discover who was the winner in this deal. It was not the US but China, the third part of the FETA menu. The American side agreed to lift most of the additional tariffs that president Trump imposed on China since his inauguration. China’s part of the deal is a vague promise to lift the restrictions on rare earth exports that it imposed on April 4. These restrictions were much better organized and more biting than the restrictions China imposed in the early 2010s. A number of American companies, and also European ones, were hit hard by these new Chinese restrictions, the sustainable energy, high tech, defense and car industries being prime examples.

Donald Trump and his advisors on trade clearly underestimated the very powerful position China occupies with respect to rare earth minerals. Technological advances have made many sectors dependent on the availability of such “exotic” minerals as amongst others neodymium, praseodymium, dysprosium, cerium, lanthanum, yttrium, europium and terbium. The simple reality of today is that China mines 70% of rare earth concentrates, processes 87% and refines 91%. Obviously the de facto stronghold on these strategically vital minerals gives the Chinese authorities leverage that is hard to counter in any trade negotiation, as Trump and his advisors found out.

“Donald Trump and his advisors on trade clearly underestimated the very powerful position China occupies with respect to rare earth minerals“

Of course China is also dependent on the American market. But … China is a +/- $ 15 trillion dollar economy and its exports to the US amount to $ 550 billion or a bit short of 4% of GDP. This is important but manageable given that China can replace its imports from the US more easily than the other way round. Moreover, there is the reality of China’s dictatorial political regime. This means that most probably higher prices and shortages of some goods due to trade tariffs are politically more explosive in the democratic West than in authoritarian China. This is also a reality that the present administration in Washington tends to overlook.

The American president might also take a lesson from the FETA he’s being served: perhaps think more carefully before announcing new policies? Assess the pros and cons, and strategic strengths and weaknesses more accurately? We can only hope.