Trump’s relentless bashing of the chairman of the American central bank is the last thing the US economy and the world at large needs at this moment. Despite recent back-pedaling by the president, the Fed’s independence remains a needle in his eye.

Imagine air traffic controllers at a major international airport abandoning all the established rules of their job and starting to transmit take-off and landing instructions in a totally random way. Consider that some of these random orders are issued even with the intention of deliberately creating collisions and other accidents. The ensuing chaos would be highly destructive, an immediate human tragedy accompanied by a sudden and dramatic loss of trust . What Donald Trump has been doing during his first 100 days of his second term as American president is comparable to what my out-of-control air traffic controllers would bring about. The major difference is that the wreckage emanating from the air controllers’ actions would be immediately visible, whereas the results from Trump’s mayhem will take time to percolate.

“I think he’s an adult”

Anybody familiar with the regular columns of Martin Wolf knows that it takes a lot before the much-respected commentator of the Financial Times starts writing about a personality like the president of the United States as “a mad king”. When Jamie Dimon, the also much-respected CEO and Chairman of JP Morgan Chase, the world’s largest bank, is trying to describe the inner workings of the Trump administration, he finally pins his hopes on Treasury Secretary Scott Bessent. Dimon’s justification is simple, but fragile: “I think he’s an adult”. The infantile, chaotic and even perversely inspired nature of most Trump policies can indeed no longer be in doubt.

Take for instance the crusade on trade tariffs. The flip-flopping on those tariffs has done as much damage as the pain the tariffs themselves would inflict. The arbitrary imposition, escalation and suspension of the tariffs has raised uncertainty for businessmen, investors and consumers, halting investment and productive endeavors. The rude attacks on the rule of law, the assaults on the attorney-general, on law firms and the threat of impeaching judges are fundamentally undermining one of the main pillars of American democracy and personal freedom, further escalating uncertainty and fear. The same can be said with respect to Trump’s brutal assaults on American universities like Harvard and Columbia, essential parts of America’s reputation for excellence and scientific advancement.

In the international geopolitical theatre too havoc and mayhem dominate as a result of the new administration’s actions. Ad hoc improvisation and contradictory initiatives have not brought peace closer in Ukraine, nor in Gaza. Nor in relations with Iran, even on the contrary. In the meantime, China is calling Trump’s bluff and ostensibly refuses to come to the trade negotiating table. The Trump presidency clearly doesn’t have a clue about how to deal with Beijing’s response to the Trump provocation. At least Scott Bessent, the “adult one”, realizes that the tariff war with China is “unsustainable”. A red line running through Washington’s external policies is total disregard, or even contempt, for allies and their needs and aspirations. Specifically, the European Union is constantly threatened with something bordering on outright hatred.

“China is calling Trump’s bluff and ostensibly refuses to come to the trade negotiating table.”

Despite all the “successes” just briefly summarized, there is a real chance that the most destructive steps the Trump administration will take, are in the financial sphere. Two elements of what the president and the members of his inner circle have been throwing around could produce extremely harmful effects, for the United States as well as for the rest of the world. First, there are the ideas promoted by Stephen Miran, the chairman of the Trump’s Council of Economic Advisors. Miran’s objectives include forcing foreign investors to accept perpetual US Treasuries and pushing down the dollar exchange rate by turning the screws further on foreign governments and investors (see also my previous blog).

Flip-flopping once more

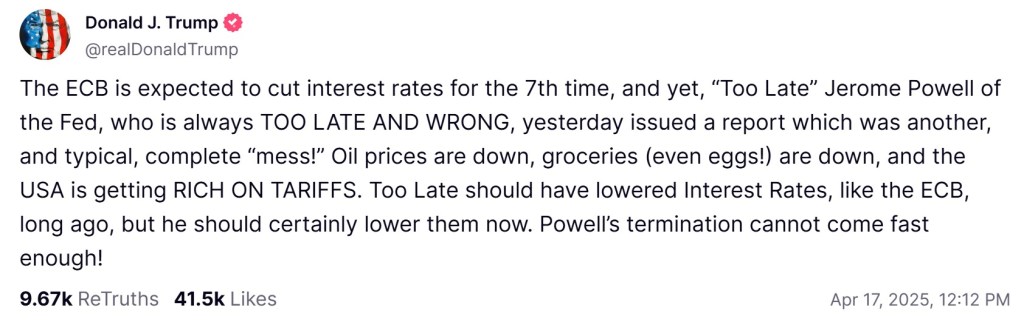

The second action in the financial realm that threatens to go nuclear concerns the Federal Reserve and more specifically its Chairman Jay Powell. Chairman Powell was, to recall, installed in February 2018 in this function by … then president Donald Trump. At that time Trump praised Powell as “strong, committed and smart”. Nevertheless, Trump is now fiercely and most brutally attacking Powell for being reluctant to start cutting American interest rates, ultimately at his behest rather than any other motivation.

The following excerpt from an April 17 post by Trump on his social media platform Truth Social gives a taste of how Trump is looking at Powell at this moment:

On other occasions the president was even more vitriolic towards Jay Powell bashing the Fed chairman as “a major loser” and “an enemy of America” in public posts.

Consternation and surprise around the world when on April 22 the president suddenly completely back-pedaled on his crusade against Powell, asserting that “I have no intention of firing him”. Trump would still like to see Powell be more active “in lowering (interest rates) but if Powel doesn’t, it is not the end”. Since flip-flopping has been the basic characteristic of the second Trump presidency, we better not take this back-pedaling as definitive. The Fed’s independence remains a reality hard to accept for this president.

On the contrary, Trump and his team better start praising Powell and the other directors at the Fed – it is a team that is taking policy decisions there, not Powell on his own – for the policies they’re pursuing. Given the evolution of inflation and inflationary expectations in the US and given too the potentially important inflationary effects of Trump’s tariff bonanza, Powel and his colleagues at the Fed are absolutely correct in their judgement to leave interest policy rates where they are.

“ Trump and his team better start praising Powell and the other directors at the Fed.”

Last man standing

Despite the recent volte-face, Trump’s basic attitude towards Powell and the Fed as an institution remain a genuine risk for the reputation of, and trust in, the Fed. If a central bank loses its reputation and trust, the credibility of monetary policies is lost. That is the main reason why most advanced countries granted their central banks independence from the day-to-day turbulence of political life. It is not disputed that the political world decides on the major appointments within central banks, like the chairman, but it is equally accepted that politicians should keep their hands off the operational management of monetary policies. History abundantly shows that leaving monetary policy directly in the hands of politicians is a recipe for financial, economic and finally also political disaster.

Let me be very clear here. I myself was regularly critical in the past of the policy lines pursued by the European Central Bank (ECB). I think it is perfectly valid for a politician to voice such criticism in a well-argued and decent way. In doing so they engage in a constructive discussion with central bank representatives. This is exactly what I did during several sessions in the European Parliament, where hearings with ECB top executives regularly take place. There is however, no doubt in my mind about the necessity for central bankers to be operationally independent of political influences. This is the mirror image of what transpires with respect to fiscal policy. Central bankers are at liberty to criticize fiscal policies pursued by governments, and several of them do so regularly. It remains ultimately up to the political world to take the decisions on fiscal policy.

The division of labor described above is not to the liking of Donald Trump. Apart from the apparent fact that this is a president who wants to have the final word on everything, Trump’s relentless bashing of Jay Powell most probably is part of the blame game Trump is starting. The American economy is slowing down with even a recession now a real possibility. Combined with a potentially upward trend in inflation, one gets a cocktail that will go down badly with the American electorate. Donald Trump will not hesitate to blame all this on Jay Powell’s policies and on Chinese strongman Xi Jinping’s refusal to come to the negotiating table. And, yes of course, the Europeans will not be spared a share of the blame.

The American president should realize that Jay Powell and the Fed are presently something like the Last Man Standing on the American economic and financial policy scene. If Powell gives in to Trump’s diatribes or if one way or another Trump finds a way to prematurely end Powell’s tenure, worse will ensure. Inflationary expectations will even more de-anchor, equities will tank further, and bond prices (bringing about higher interest rates) and the dollar will sink deeper. In an arena built on trust, bashing (or even liquidating) Powell is the surest way to destroy what is left of belief in the American financial system.